Best and Cheapest Home Insurance Companies in Connecticut (2026)

State Farm sells the best and cheapest home insurance for most people in CT, with an average rate of $1,091/yr for $350,000 in coverage. | ||

Connecticut home insurance costs an average of $2,346/yr, which is close to the national average. | ||

Homeowners in southen Connecticut pay the highest average rates in the state. A $350,000 policy in New Haven costs $3,133/yr. |

State Farm sells the best and cheapest home insurance for most people in CT, with an average rate of $1,091/yr for $350,000 in coverage. | ||

Connecticut home insurance costs an average of $2,346/yr. Homeowners in New Haven pay an average of $3,133/yr. |

Find Cheap Home Insurance Quotes in Connecticut

Who has the best cheap home insurance in Connecticut?

What company has the cheapest homeowners insurance in Connecticut?

State Farm has the cheapest home insurance for most people in CT. A State Farm policy with $350,000 in dwelling coverage costs $1,091 per year, on average.

Find Cheap Home Insurance Quotes in Connecticut

- Along with State Farm, you can frequently get cheap home insurance rates in Connecticut from Amica, Mapfre and Allstate.

- State Farm also has the cheapest rates for new homes at $579 per year.

- If you have a high-value home, consider Chubb. You'll pay more for coverage, but the company has coverage options specifically tailored to the needs of luxury houses.

Home insurance quotes in Connecticut by dwelling limit

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| State Farm | 3.5 out of 5 | $761 | |

| Amica | 5.0 out of 5 | $1,132 | |

| Mapfre | 3.3 out of 5 | $1,322 | |

| Allstate | 4.0 out of 5 | $1,406 | |

| Narragansett Bay | 4.5 out of 5 | $1,417 |

| Andover | 4.0 out of 5 | $1,511 |

| Progressive | 2.0 out of 5 | $2,983 | |

| American Family | 2.5 out of 5 | $3,107 | |

| USAA* | 4.5 out of 5 | $907 | |

*USAA is only available to military members, veterans and some of their family members.

Key takeaways

- Home insurance rates in CT have gone up by about 38% over the last five years.

- Nationwide has raised rates by nearly 65% since 2021, the most of any company in Connecticut.

- Amica has had the smallest increase since 2021. Its policies cost about 7% more than they did five years ago.

Best home insurance in Connecticut for most people: State Farm

-

Annual cost$1,091Average rate for a $350,000 home

-

Monthly cost$91Average rate for a $350,000 home

-

Customer complaints Average

State Farm is the cheapest home insurance company in Connecticut.

At $1,091 per year, a policy with $350,000 of dwelling coverage is less than half of the state average. And if you need more coverage, State Farm is still a cheap choice.

State Farm is also a great choice for most people because it has cheap car insurance rates in Connecticut. And on top of its cheap car and home insurance rates, State Farm has a good bundling discountthat can save you even more. On average, you can save about 27% on your home insurance and 18% on your car insurance by bundling with State Farm.

All you have to do to get the bundling discount is buy both your car and home insurance from State Farm.

State Farm has local agents in 83 Connecticut cities, which means it's likely there's an agency near you. Working with a local agent can be helpful. Agents understand the unique risks that homes in Connecticut are up against and can help you pick your home insurance coverage wisely.

Best home insurance customer service in CT: Amica

-

Annual cost$1,749Average rate for a $350,000 home

-

Monthly cost$146Average rate for a $350,000 home

-

Customer complaints Low

Best home insurance in CT for flood coverage: Narragansett Bay

-

Annual cost$2,242Average rate for a $350,000 home

-

Monthly cost$187Average rate for a $350,000 home

-

Customer complaints Low

Narragansett Bay offers flood protection on its home insurance policies, making it the best choice for homes along the coast or near a river.

You usually have to buy a separate flood insurance policy to have coverage for flood damage. But Narragansett Bay offers flood coverage as a home insurance add-on. And you can get coverage for the full value of your house, which is a huge perk.

With Narragansett Bay's flood coverage add-on, you'll get the same amount of flood protection for your home and belongings as you would for other types of damage, like a fire. This can be great for people with expensive homes who can't get enough coverage from the National Flood Insurance Program (NFIP).

Having your home and flood insurance policies with the same company will also make your life easier if you ever have to file a claim. That's because you'll only need to work with one company and one adjuster.

Narragansett Bay also has cheap rates. A policy with $350,000 in dwelling coverage costs an average of $2,242 per year with Narragansett Bay, which is 4% cheaper than the state average. And Narragansett Bay has good customer service too, with around one-fourth the number of complaints expected for a company its size, according to the National Association of Insurance Commissioners (NAIC).

What are the best-rated home insurance companies in CT?

Amica and Narragansett Bay are high-rated home insurance companies in Connecticut.

Both companies have very few customer complaints, according to the National Association of Insurance Commissioners (NAIC). That means their customers are generally satisfied with their service.

Amica also has excellent scores on J.D. Power's home insurance survey and its property claims survey. J.D. Power did not rate Narragansett Bay because it focuses on large, national companies.

Company |

Rating

|

Complaints

|

|---|---|---|

| Amica | 5.0 out of 5 | Low |

| Narragansett Bay | 4.5 out of 5 | Low |

| USAA | 4.5 out of 5 | Low |

| Allstate | 4.0 out of 5 | Average |

| Andover | 4.0 out of 5 | Low |

| State Farm | 3.5 out of 5 | Average |

| Mapfre | 3.3 out of 5 | Average |

| Chubb | 3.0 out of 5 | Low |

| American Family | 2.5 out of 5 | Average |

| Progressive | 2.0 out of 5 | Average |

How much does Connecticut homeowners insurance cost?

The average cost of home insurance in Connecticut is $2,346 per year for $350,000 in dwelling coverage.

That's in line with the national average, which is $2,395 per year.

Average cost of Connecticut home insurance by dwelling amount

Dwelling coverage | Average rate |

|---|---|

| $200,000 | $1,616 |

| $350,000 | $2,346 |

| $500,000 | $3,157 |

| $1 million | $5,530 |

Home insurance in Connecticut is more expensive than it is in the nearby states. For example, home insurance in New York costs $1,387 per year, while coverage in Massachusetts costs $1,635 per year. That could be because Connecticut's southern coastline exposes much of that state to strong coastal storms.

Connecticut homeowners insurance rates by city

Westbrook Center, along the southern coast of CT, has the most expensive home insurance rates in the state, at $3,463 per year for $350,000 in dwelling coverage.

This is likely because its position on the coast makes it more vulnerable to damage from coastal storms. You typically pay less if you live in the more northern areas of Connecticut. Amica is a cheaper option in Westbrook Center, with a policy coming in at $2,257 per year, on average.

Unionville, to the west of Hartford, has the cheapest home insurance in Connecticut. A $350,000 policy in Unionville costs $1,939 per year, on average.

Find Cheap Home Insurance Quotes in Connecticut

CT homeowners insurance rates by city

City | Average rate | Cheapest company | Cheapest rate |

|---|---|---|---|

| Abington | $2,053 | Amica | $1,486 |

| Amston | $1,995 | State Farm | $668 |

| Andover | $2,023 | State Farm | $586 |

| Ansonia | $2,372 | State Farm | $572 |

| Ashford | $1,984 | State Farm | $558 |

| Avon | $1,960 | State Farm | $553 |

| Ballouville | $2,064 | Amica | $1,486 |

| Baltic | $2,260 | State Farm | $693 |

| Bantam | $2,024 | State Farm | $535 |

| Barkhamsted | $2,019 | State Farm | $525 |

| Beacon Falls | $2,340 | State Farm | $545 |

| Berlin | $2,019 | State Farm | $662 |

| Bethany | $2,521 | State Farm | $551 |

| Bethel | $2,018 | State Farm | $500 |

| Bethlehem | $2,000 | State Farm | $536 |

| Bethlehem Village | $1,999 | State Farm | $533 |

| Bloomfield | $2,071 | State Farm | $678 |

| Blue Hills | $2,069 | State Farm | $662 |

| Bolton | $1,990 | State Farm | $558 |

| Botsford | $2,253 | Amica | $1,518 |

| Bozrah | $2,399 | State Farm | $665 |

| Branford | $3,071 | State Farm | $1,468 |

| Branford Center | $3,073 | State Farm | $1,468 |

| Bridgeport | $2,806 | State Farm | $1,312 |

| Bridgewater | $2,022 | State Farm | $527 |

| Bristol | $1,970 | State Farm | $537 |

| Broad Brook | $2,068 | State Farm | $662 |

| Brookfield | $2,068 | State Farm | $504 |

| Brooklyn | $1,942 | State Farm | $666 |

| Burlington | $2,012 | State Farm | $549 |

| Byram | $2,333 | State Farm | $1,185 |

| Canaan | $2,016 | State Farm | $517 |

| Canterbury | $1,963 | State Farm | $680 |

| Canton | $2,008 | State Farm | $532 |

| Canton Center | $2,134 | Narragansett Bay | $1,462 |

| Canton Valley | $2,009 | State Farm | $543 |

| Centerbrook | $2,698 | State Farm | $960 |

| Central Village | $1,947 | State Farm | $693 |

| Chaplin | $1,967 | State Farm | $655 |

| Cheshire | $2,323 | State Farm | $586 |

| Cheshire Village | $2,322 | State Farm | $577 |

| Chester | $2,499 | State Farm | $833 |

| Chester Center | $2,500 | State Farm | $827 |

| Clinton | $3,298 | Amica | $2,257 |

| Cobalt | $2,818 | Amica | $1,565 |

| Colchester | $2,409 | State Farm | $657 |

| Colebrook | $2,037 | State Farm | $525 |

| Collinsville | $2,009 | State Farm | $544 |

| Columbia | $1,999 | State Farm | $668 |

| Conning Towers Nautilus Park | $3,131 | State Farm | $1,294 |

| Cornwall Bridge | $2,016 | State Farm | $524 |

| Cos Cob | $2,367 | State Farm | $852 |

Rates are for a policy with $350,000 of dwelling coverage.

What home insurance coverage do you need in Connecticut?

Connecticut is a coastal state with lots of rivers, which means many homes across the state are at risk of flood damage. In addition, heavy wind and rain from nor'easters can cause significant damage to coastal homes.

Does Connecticut home insurance cover flooding?

Homeowners insurance typically doesn't cover weather-related flood damage.

You usually have to buy a separate flood insurance policy to get coverage, unless your company offers an add-on, like Narragansett Bay. If you live in an area with a high risk of flooding, your mortgage company may require you to have flood insurance.

The southwest corner of Connecticut, which borders the Long Island Sound, is at the highest risk of flooding in the state. But flooding can and does happen anywhere in Connecticut. Since 2015, the National Flood Insurance Program (NFIP) has handled nearly 1,500 flood claims in the state, which caused almost $52 million in damage.

Even if you're not in a high-risk flood zone, you may want to consider getting flood insurance. That's because just one inch of floodwater can cause around $25,000 of damage to your home, according to the Federal Emergency Management Agency (FEMA).

Connecticut homeowners can get flood insurance through the National Flood Insurance Program (NFIP) or a private insurance company. In addition, some Connecticut home insurance companies, like Narragansett Bay, sell flood insurance as an add-on to your home insurance policy.

Does home insurance in CT cover wind damage?

Homeowners insurance usually pays for damage caused by high winds.

This includes everything from thunderstorm winds to hurricane-force winds. Storm winds could blow off roof shingles or siding, or cause a tree to fall on your home.

Connecticut isn't the windiest state in the country, but it sees its fair share of windstorms. In 2025, the state had 69 windstorms, according to the NOAA/National Weather Service Storm Prediction Center.

If your home is near the coast or in an area with frequent high winds, your insurance policy may have a separate wind deductible. This deductible is usually between 1% and 5% of your dwelling coverage limit.

How to get the best homeowners insurance in Connecticut

To find the best home insurance company for you, shop around for quotes, compare coverage options and consider customer feedback.

There's a difference of $3,249 per year between the most and least expensive home insurance companies in CT. That's because each company calculates rates differently. Shopping around lets you see all your options and helps you find the best cheap policy for you. | |

Most basic home insurance policies are fairly similar. However, a standard policy may not offer enough coverage for you. In that case, it's important to find a company that has the right mix of coverage add-ons to fully protect your home. For example, if you have a high-value home, Chubb could be a good choice because its policies are specifically designed for expensive homes. Or, if your home is near a river or the Atlantic coast, you might consider Narragansett Bay for its flood insurance coverage. | |

You should be able to count on your home insurance company to take care of you if your home is ever damaged. Companies with excellent customer service reviews are more likely to have an easy claims process and help you repair your home quickly. On the other hand, poor customer service could lead to a lot of back and forth with the insurance company. And, you could end up paying more to fix your house. |

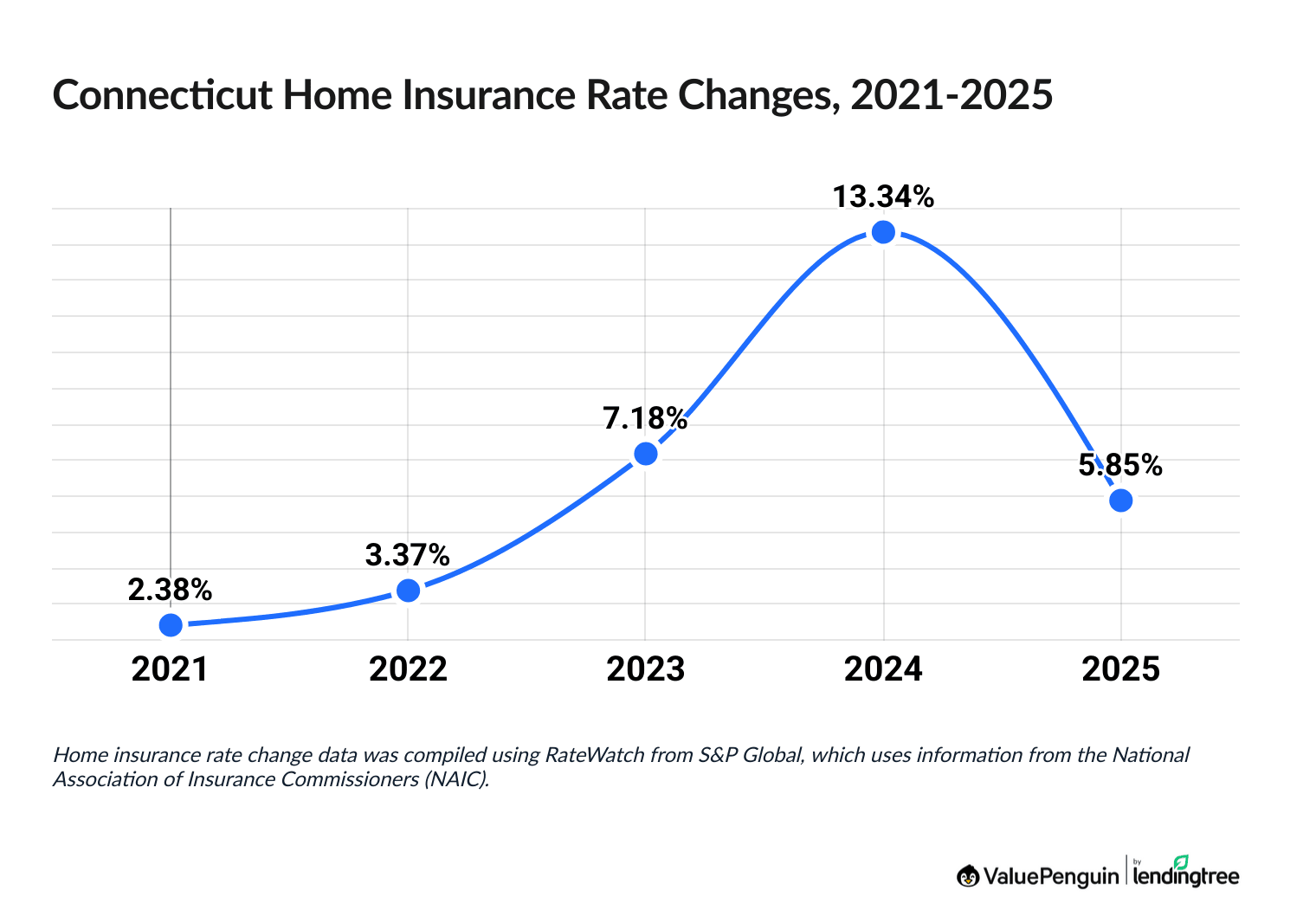

Are home insurance rates going up in Connecticut?

Home insurance rates in Connecticut have gone up by about 38% over the last five years.

The largest increase was in 2024, when rates went up by about 13%.

Connecticut home insurance rate increases, 2021-2025

Year | Avg. rate increase |

|---|---|

| 2021 | 2.38% |

| 2022 | 3.37% |

| 2023 | 7.18% |

| 2024 | 13.34% |

| 2025 | 5.85% |

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Nationwide had the largest increase, with rates going up by nearly 65% since 2021.

Amica's rates have been the steadiest. A policy with Amica costs about 7% more now than it did five years ago.

Frequently asked questions

What is the average home insurance cost in CT?

Home insurance costs an average of $2,346 per year in Connecticut. That's close to the national average of $2,395

What is the best home insurance in Connecticut?

State Farm has the best home insurance for most people in Connecticut because of its low monthly rates, reliable customer service and availability.

What is the cheapest home insurance in Connecticut?

State Farm has the cheapest rates in Connecticut at $1,091 per year for a $350,000 policy. That's about 53% below the state average. Other cheap companies include Allstate and Amica.

Does CT require home insurance?

Home insurance isn't legally required in Connecticut. However, if you have a mortgage, your lender typically requires you to buy a policy.

Methodology

To find the best home insurance in Connecticut, ValuePenguin collected quotes from 10 of the top home insurance companies in the state in every residential ZIP code. Rates are for a 45-year-old married man with good credit and no prior home insurance claims. Rates are for a 2,158 square foot house built 56 years ago. This aligns with the average home in Connecticut. New home data is for a home built in 2025.

Quotes include the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $1,000

- Deductible: $1,000

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurance company filings and should be used for comparative purposes only. Your own quotes may be different.

Home insurance ratings are based on complaint data from the National Association of Insurance Commissioners (NAIC), the J.D. Power customer satisfaction survey, as well as ValuePenguin's ratings from the editorial staff.

Sources:

About the Author

Senior Writer

Cate Deventer is a Senior Writer who specializes in health insurance, Medicare, auto and home insurance. She's been a licensed insurance agent since 2011.

She started her insurance career working as a customer service agent for State Farm. She later moved to an independent agency, where she worked with several insurance companies and hundreds of clients. She quoted policies, filed claims and answered insurance questions. In 2021, she pivoted her career and began writing about insurance for Bankrate. She moved to ValuePenguin in 2023 and began writing about health insurance and Medicare.

Cate has a passion for helping readers choose insurance to fit their needs. She enjoys knowing that her research and knowledge help people choose insurance products that make a positive difference in their lives.

How insurance helped Cate

Cate used her health insurance knowledge to navigate a surgery in 2023. Understanding how her policy worked let her focus on recovery instead of worrying about bills.

Expertise

- Health insurance

- Medicare & Medicaid

- Auto insurance

- Home insurance

- Life insurance

Credentials

- Licensed Life, Accident & Health Insurance Agent

- Licensed Property & Casualty Insurance Agent

Referenced by

- CBS

- NBC

- Wall Street Journal

Education

- BA, Theatre, Purdue University

- BA, English, Indiana University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.